Early Stage Investing - 2023

Early Stage Investing - 2023

Back to Fundamentals

How do you invest in early stage startups in 2023? Last week, HERmesa was lucky enough to learn from three fantastic investors about how they see the pre/seed markets evolving over the next twelve months.

Many thanks to:

Andrea Sinclair, UKBAA Angel Investor of the Year

Claire Cherry, Investment Partner at Joyance Partners

Gloria Baeuerlein, Angel Investor, Germany

for sharing their insights with us. Read on to learn what they said….

Setting the Scene

2022 was a tough year for both public and private technology investments.

The tech heavy NASDAQ index was down 34%, late stage private market financing valuations fell off of a cliff - e.g. median valuations are down 50% for Series B companies -and the IPO market effectively closed.

Early stage businesses managed to buck this trend in the first half of 2022, in part, buoyed by multi-stage funds, keen to deploy capital, moving into seed & series A deals.

But, by 3Q 2022 the downturn had hit early stage startups as well.

Atomico’s “State of European Tech - 2022” reports that early stage financing volumes fell by ~30%

And Angel List’s annual report on the state of U.S. early stage businesses seconds this, noting that:

In 3Q22, turbulence in the broader market trickled down to the early-stage market in a major way, with deal volume and positive activity dropping to levels not seen since the onset of the pandemic

But, while the market has slowed, it certainly has not stopped for early stage investments. Capital - both individual (angel) and institutional (funds) - is still available, companies are still raising ‘up’ vs. ‘down’ rounds (more on Valuation below) and as Claire Cherry said:

"This is a much more positive time to be investing. Everyone says that recessions are the golden age of investing (even if it doesn’t feel like it sometimes!). At this point in the cycle, you can get to know founders and businesses better and you can get into companies on better terms with better valuations.”

So, how should I invest in 2023?

TL;DR: same as it ever was: Focus on Founders; Business Fundamentals; “Drugs vs Vitamins”…but take more time to diligence the companies.

All three investors took pains to emphasise that the basics of early stage investing have not changed at all. You should deploy capital into

Exceptional Founders: particularly those who are serial entrepreneurs and/or operators with deep experience (“you are the best customer for the solution that you are building”)

Businesses that make sense: In the past few, frothy years, companies were able to raise that really didn’t have a sense of product/market fit or how to make the margins eventually work. There is a return to backing founders who deeply understand the right metrics to drive their business from the beginning, as well as those founders who are focusing on managing cash, including having a credible Plan B if they are unable to raise the next financing round.

Drug vs Vitamin: In VC, there is a common question: “Is your product/service a drug or a vitamin?” This is a shorthand to ask whether or not your company is solving a real problem for its target customers (i.e. it requires a ‘drug’ to cure the pain). If the problem is not “painful” enough or it is a ‘nice to have’ for your target customers, it is likened to a ‘vitamin’; spending for which will be cut during a recession. It goes without saying that as an investor, you want your portfolio to be full of drugs, not vitamins!

Valuation

What is going on with valuations in this market?

With the IPO market effectively closed, investors have no idea of the ‘right’ exit multiples to apply to their later stage businesses, and this is cascading into the earlier stages with many companies seeing a decline in valuation vs 2021/early 2022 numbers. But, the story is more nuanced…

Gloria Baeuerlein explained that current valuations for early stage companies can be split into three buckets:

“Best of the Best” - for the top 1-2% of extraordinary founders, with easy to understand businesses that tick a lot of the boxes for early stage investors (particularly those multi-stage funds moving into pre/seed), valuations have not changed from 2021/22 levels.

Really Good Startups - companies with really good founders, strong product market fit and solid traction are still raising pre/seed rounds, albeit at valuations that are about 20-30% off of 2021/22 levels. Rather, the valuations are closer to 2019 metrics. Gloria estimates that there are 40-50% of startups who fall into this bucket.

Struggling Startups - for the bottom half of the market, it is very difficult. These companies are struggling to raise and this can be for a variety of reasons: maybe the companies require too much capital to grow (e.g. therapeutics) or the companies have yet to find product/market fit or the founder has a poor grasp on metrics / finances.

The trick for investors is to review all companies dispassionately - especially if they are already in your portfolio!

A final comment on valuations….

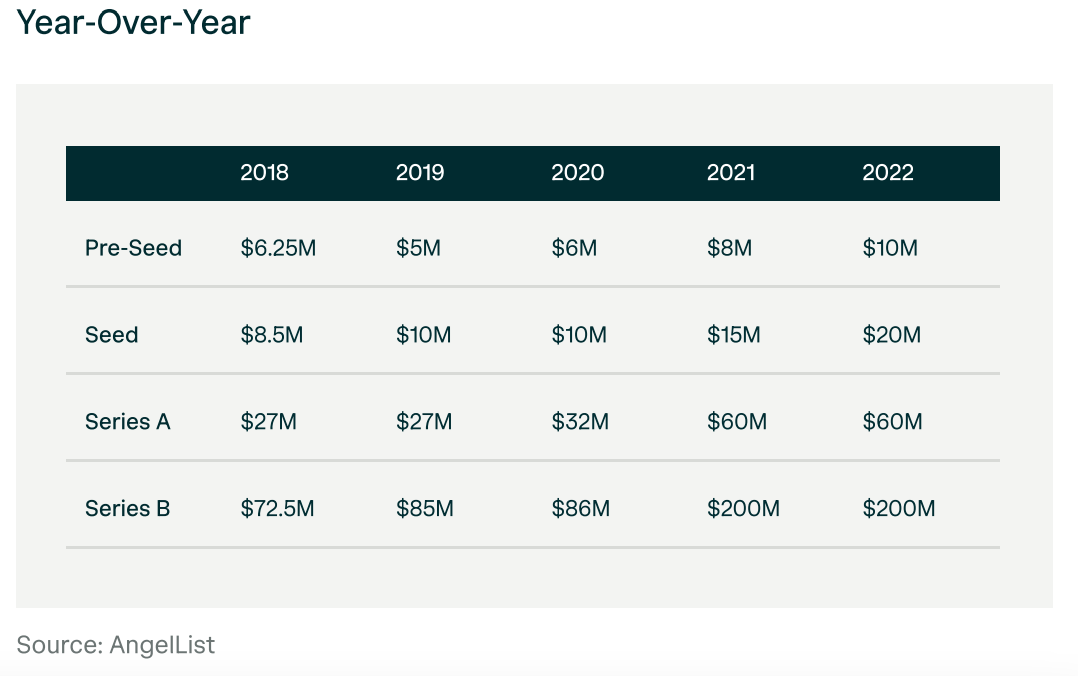

All investors agreed that there is a re-indexing of fair value after the market euphoria of the last few years. Investors are still struggling to find the ‘right’ value, but there is a sense it will be around 2018/19 levels. What does that mean in practice? The market still has a ways to fall before it stabilises. The chart below shows median valuations by stage:

Bridge Rounds / ASAs / Converts

Against all of the market uncertainty, investors are being asked to invest via convertible notes and ASAs (a UK specific convertible note). We are also seeing a number of our portfolio companies come to us for “bridge rounds” - just enough money to get to “X” metric, at which point the companies ‘can raise at a higher valuation’.

Andrea Sinclair made a number of very good points about how she thinks about these instruments:

An ASA is a priced round by any other name. It needs to convert within 6 months in order to qualify for EIS tax treatment (unless companies raise a priced round in the intervening period - which is unlikely to be the case). So, you are essentially buying common stock at the ‘longstop’ valuation expressed in the ASA but not getting any of the investor protections that you might otherwise receive while investing in a regular convertible note. Think about an ASA + tax relief vs a convertible note, without the tax relief if you are a UK investor!

A convertible note with a discount to the subsequent priced round (but not an automatic conversion to equity) is a reasonable way of dealing with longer term valuation uncertainty.

Bridge Rounds - dig deeply into the use of funds with the founder. If she/he doesn’t manage to raise that next round, then what happens? Is there a plan B?

At HERmesa, we remain excited about the early stage investment opportunities in 2023. There are still companies building exciting solutions to hard problems…but we are following this expert advice in being thoughtful about how we invest.

We’re keen to see the year play out!